PCI Reinsurance Panel

At the 2017 PCI Annual Meeting, a panel discussed the state of the global reinsurance market and what to expect in 2018. The panel included:

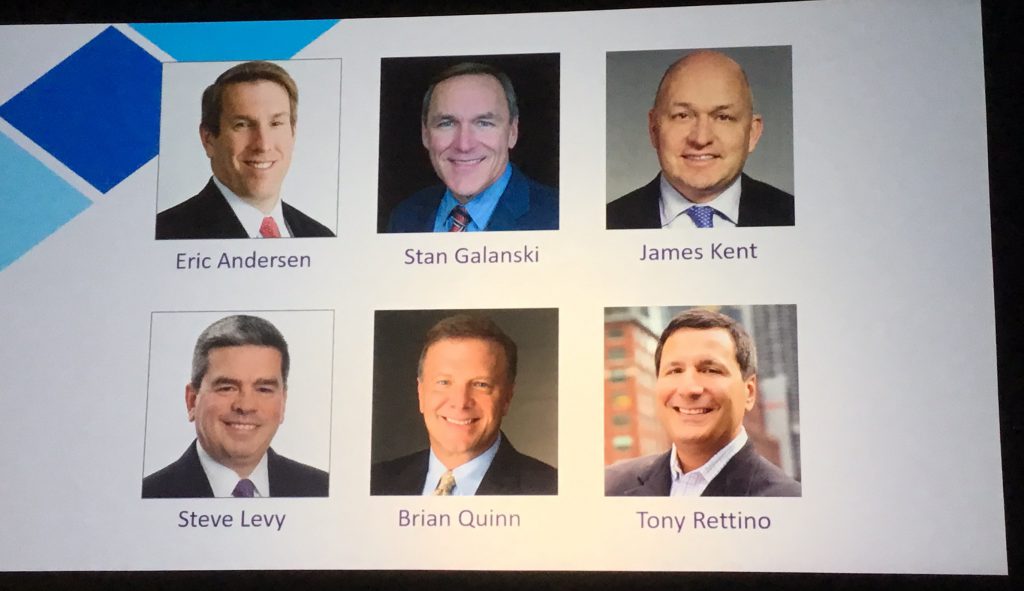

- Stan Galanski – President and CEO, The Navigators Group, Inc.

- Eric Anderson – CEO, AON Benfield

- James Kent – Global Deputy CEO & North America President, Willis Re

- Steve Levy – President, Reinsurance, Munich Re America

- Brian Quinn – CEO of North America, Odyssey Re

- Tony Rettino – Founding Principal, Elementum Capital

Q: Where is the reinsurance market heading for at the 01/01 renewal?

Answers:

Don’t buy into the hype. Ultimately the market is made up of individual customers that want to be evaluated on their own merits.

There have been a large amount of CAT events, but this is about more than that. The market is always looking at whether they are receiving adequate premiums for the risks they are taking.

It is realistic to expect some upward movement in rates based on circumstances the way they are. The underlying economics suggest where the market will be going.

In the last quarter, roughly $100 billion left our industry. It’s hard to see that leading to anything but a meaningful change in rates.

We rely on the accuracy and predictive power of the models. What the losses in the last quarter have shown is that there is more uncertainty in terms of potential losses.

Differentiation between companies is important. Some companies have performed better than others and you should not lump everyone together.

Q: How much will the retro market drive pricing behavior?

Answers:

Pricing in the retro market has declined in recent years. The retro market has the most uncertainty. Most retro markets have been hit by these CAT events.

People are coming out of these events not equal. We expect to see variation in the approach.

The market is functioning as it should. To provide customers with the support they need.

Alternative capital is heavily invested in the retro market, and they have tended to rely on the CAT modeling. If their faith in these models waivers, that capital may be redeployed outside of the insurance industry.

You cannot be overly reliant on the models. Good old fashioned underwriting still matters.

Funds that performed as expected have ample capital ready to invest in them.

Reinsurance has become a recognized asset class for pension funds. This will not change.

Q: Will there be differentiation between carriers and reinsurers in how they respond to this year’s events?

Answers:

Different carriers have a different mix of business so there is variation in the impact.

This year’s events will wipe out earnings and even capital assets for some.

Although in some cases these events were like never seen before, that does not mean they were unanticipated.

We won’t know if there are any surprises in the ultimate losses associated with these events until several years from now. Expect significant litigation especially in Texas.

Q: What is the implication of Hurricane Harvey on development of a private market for flood insurance?

Answers:

75% of the economic losses for Harvey will be uninsured. That highlights a need for the private marketplace to enter the flood market.

Harvey exceeded flood models which is causing some carriers to pause on thoughts of entering the flood insurance marketplace.

For the private marketplace to replace the government for flood insurance, pricing and modeling has to improve.

The government will always have a role in flood insurance. Perhaps as a stop loss market.

Our industry needs to better educate the general public on the need for flood insurance. What is covered and what is not under their standard homeowners.

We need better flood mapping. Houston was not designated as a flood zone even after a prior hurricane caused flooding.

Pricing for flood insurance needs to better represent the risk. Coastal property should cost more than inland property.

Q: Is there a change coming in the pricing for the casualty market?

Answers:

Commercial auto has not been profitable for many years. Distracted driving is a factor. There are also more cars on the road. High tech replacement parts are very expensive to replace.

Liability awards from juries have been increasing. Plaintiff attorneys are getting more creative and are being successful.

The casualty marketplace has been propped up in recent years by the lack of property losses. These casualty lines need to stand on their own with regard to pricing.

The challenge insurers and reinsurers have had is the significant upward movement in jury awards and settlements. Current pricing is not sustainable with these award levels.

Safety National is a proud sponsor of Kids' Chance of America, a charity that provides need-based educational opportunities and scholarships for the children of workers seriously injured or killed on the job.

Search By Month

Recent Posts

- Reefer Madness: Still in the Weeds with Medical Marijuana and Workers’ Compensation

- Reshaping the Energy Insurance Market

- There Is No Spoon: How Website Tracking Technologies Spark Litigation

- Managing AI Risks When Onboarding Vendors

- How Leaders and Risk Professionals Can Navigate Challenges Together